EMI Culture in India is no longer just a repayment system — it has quietly become a lifestyle. From smartphones to homes, travel bookings to education loans, monthly instalments now shape how India consumes, aspires, and plans its future.

But is this convenience building financial stability — or slowly increasing invisible pressure? Let’s understand the deeper reality.

What Is EMI Culture in India?

EMI Culture in India refers to the growing trend of purchasing goods and services through Equated Monthly Installments rather than upfront payments.

What once applied mainly to homes and vehicles now covers:

- Mobile phones

- Electronics

- Travel

- Lifestyle products

- Education

- Even groceries in some cases

Credit has become fast, digital, and instantly accessible. For many young earners, their financial journey begins not with savings — but with borrowing.

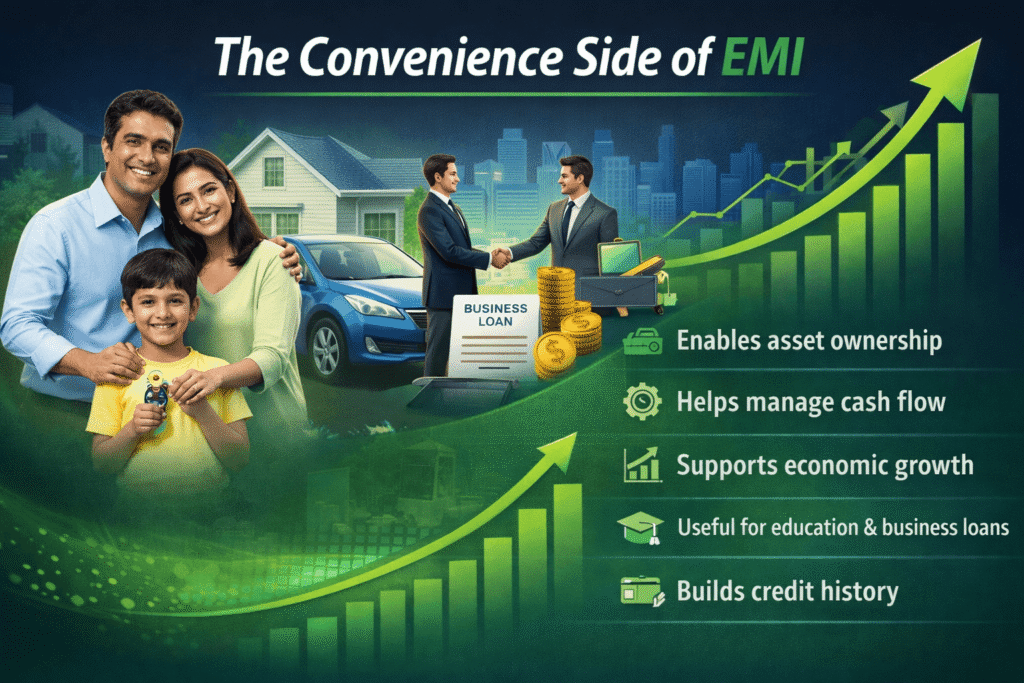

Why EMI Feels Convenient

EMI works because it reduces psychological friction.

Instead of paying ₹60,000 at once, ₹2,999 per month feels easier. That small number makes affordability look manageable.

EMIs also:

- Enable asset ownership

- Help manage cash flow

- Support education and business growth

- Build credit history

In a growing economy like India, credit supports consumption and development. Used responsibly, EMI can accelerate progress.

Convenience is real. But so is the cost.

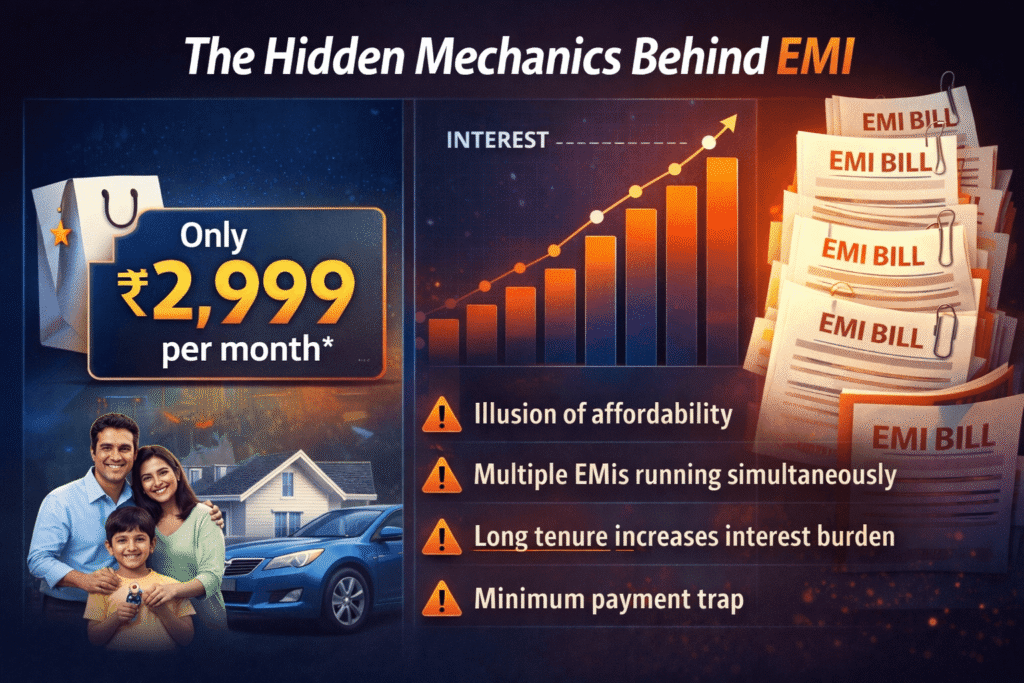

The Hidden Cost Behind Small Monthly Payments

The biggest illusion in EMI Culture in India is the “small amount mindset.”

When consumers focus only on monthly payment, they often ignore:

- Total interest paid

- Processing charges

- Long tenure impact

- Multiple EMIs running together

A longer tenure lowers EMI — but increases total repayment.

“0% EMI” often shifts cost into product pricing or hidden fees. Money always has a cost. What feels affordable monthly may become expensive over years.

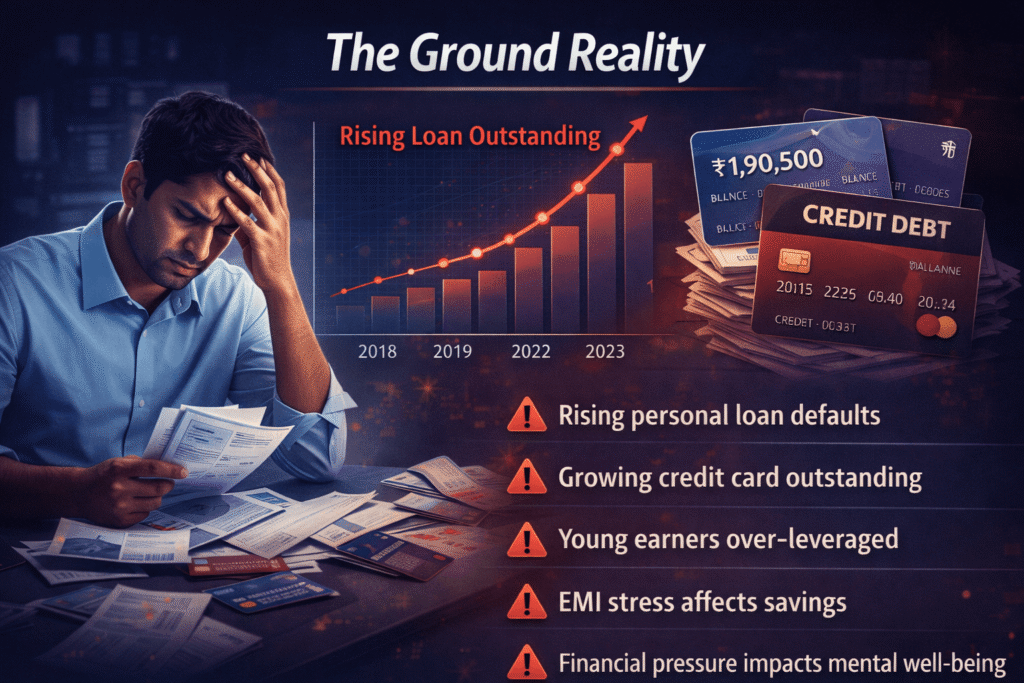

The Ground Reality of Rising Credit

India has seen a steady rise in:

- Personal loan outstanding

- Credit card usage

- Buy Now Pay Later adoption

- Early credit exposure among youth

Retail lending has grown significantly in recent years, driven by increasing consumer demand for housing, personal, and lifestyle financing.

While growth is not negative in itself, rising defaults and repayment stress indicate that financial literacy has not grown at the same pace as access to credit.

EMI Culture in India is expanding faster than financial discipline.

When Does EMI Become a Debt Trap?

EMI becomes risky when:

- EMI exceeds 40–50% of monthly income

- There is no emergency fund

- Borrowing is done for lifestyle image

- New loans are taken to repay old loans

Debt trap is not caused by EMI alone. It happens when repayment capacity is weaker than financial ambition. Consumption-based loans without long-term value often create stress rather than stability.

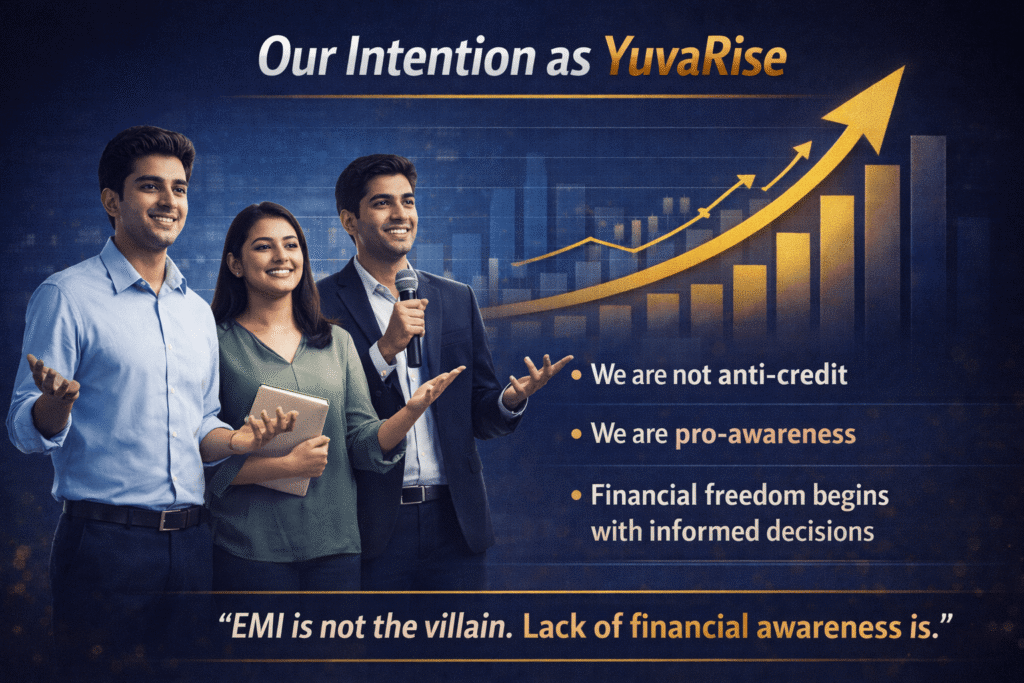

Our Balanced View: Credit Is Not the Villain

It is important to say this clearly:

EMI is not the villain. Credit has helped millions own homes, pursue education, and start businesses. It fuels economic growth and opportunity.

The real issue is not borrowing — it is borrowing without awareness.

EMI Culture in India becomes harmful only when decisions are driven by:

- Social comparison

- Marketing influence

- Instant gratification

- Lack of financial planning

Responsible credit builds assets.

Irresponsible credit builds pressure.

Financial Awareness Is the Real Power

Before taking any EMI, every young earner should ask:

- Do I have 6 months of emergency savings?

- Is this purchase a need or lifestyle upgrade?

- What is the total repayment amount?

- What happens if my income stops?

Financial freedom does not begin with earning more. It begins with understanding more.

EMI Culture in India will continue to grow. The question is — will financial awareness grow with it?

At YuvaRise, we believe progress and prudence must go together. Credit is a tool. Wisdom determines whether it builds your future — or burdens it.

If this perspective helped you think differently about money and responsibility, explore more awareness-driven insights on our Blogs.